5 min read

Buying a car is exciting, until you see the interest rate. But don't worry, scoring a low APR isn’t just for financial wizards or expert negotiators. With a little planning and the right strategy, you can land a solid deal and save thousands over the life of your loan. Let’s walk through how to get a low interest rate on a car loan, and tackle some common questions along the way.

Check your credit score first

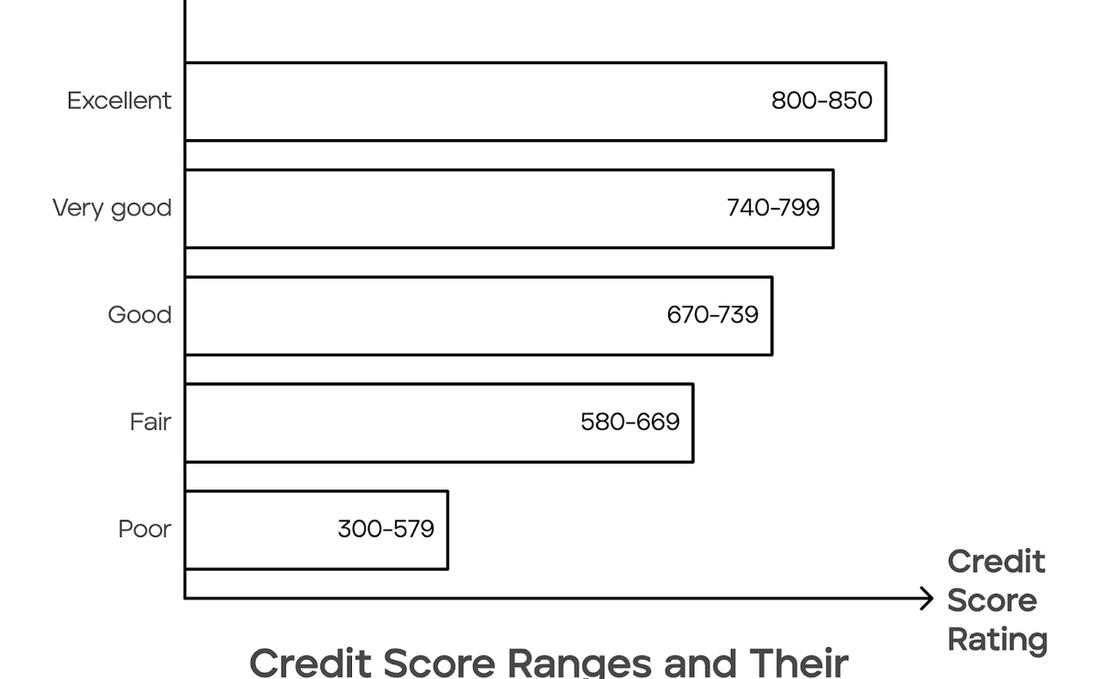

Your credit score is one of the biggest factors lenders use to determine your rate on your loan. The better your score, the better your loan terms. Run a credit report to see if you have good or bad credit. Here's a general breakdown:

- 800–850: Excellent (you’ll likely snag the lowest rates available)

- 740–799: Very good

- 670–739: Good

- 580–669: Fair

- 300–579: Poor

If you’re not in the top tiers, don’t sweat it, you can work on boosting your score before applying. Start by paying your bills on time, keeping credit card balances low, and avoiding new credit checks before applying for a loan.

Can I negotiate my car loan interest rate?

Absolutely. You can often negotiate interest rates, they aren’t always set in stone. If you have good credit, a steady income, or competing loan offers from other lenders, you’ve got leverage.

Request your lender to match or beat another offer, especially if you have received pre-approval elsewhere. A difference of even 1% in your APR can save you hundreds (or even thousands) over time.

Shop around and compare lenders

Never take the first loan offer you see. Compare quotes from banks, credit unions, online lenders, and even the dealership's financing department. Some lenders might cut you a better deal if you’re going with a shorter loan or certain types of cars.

Get quotes from at least three lenders, and check if they allow loans for buying from a private seller. Most pre-approvals involve a soft credit check, so your score won’t take a hit while you’re comparing.

Shorter loan terms can save you more

Longer loan terms might have lower monthly payments, but you’ll usually pay more in interest overall. If your budget allows, go for the shortest loan term you can afford. Paying a little more each month now can mean paying way less in the long run.

Make a bigger down payment

The more you put down upfront, the less you’ll need to borrow, and that can help you qualify for a lower interest rate. Aiming for a 20% down payment is a good rule of thumb. It shows lenders you’re a serious buyer and reduces their risk, which can translate into better rates for you.

Do you have a car to trade in? Don’t settle for the dealer’s lowball offer. Use Peddle to get an instant, no-hassle quote and see how much your current car is worth. Sell it to us and use the cash toward your down payment.

What is a good APR for a car loan?

APR (Annual Percentage Rate) varies depending on your credit score, loan term, and the lender. But here’s a ballpark:

- Excellent credit: 3% or lower

- Good credit: 4%–6%

- Fair credit: 7%–10%

- Poor credit: 11% or more

New car loans tend to have lower APRs than used car loans, but it depends on the lender and your credit profile.

Does refinancing hurt your credit?

Refinancing your car loan can temporarily lower your credit score because of the hard inquiry. Refinancing can improve your credit over time. This is especially true if it lowers your payments and helps you pay off your loan faster. If you’re stuck with a high APR, it’s worth looking into refinancing after six to twelve months of on-time payments.

Consider using a co-signer

If your credit score isn’t great, bringing in a co-signer with strong credit can help you qualify for a better interest rate. Lenders see less risk when someone with solid financials backs your loan. Just make sure your co-signer understands they’re on the hook if you miss payments. This is a significant favor, so treat it that way.

Ready to buy smarter?

Getting a low interest rate on a car loan is all about preparation. Check your credit, shop around, negotiate with confidence, and don’t be afraid to say no to a bad deal.

And if you’ve got a car to sell first, we can help. At Peddle, we give you a real offer in seconds, no pressure, no haggling, and free pickup included. The easiest way to get extra cash for your down payment is through this method.

Curious about your car’s value? Learn its current market worth with a quick and easy online estimate.